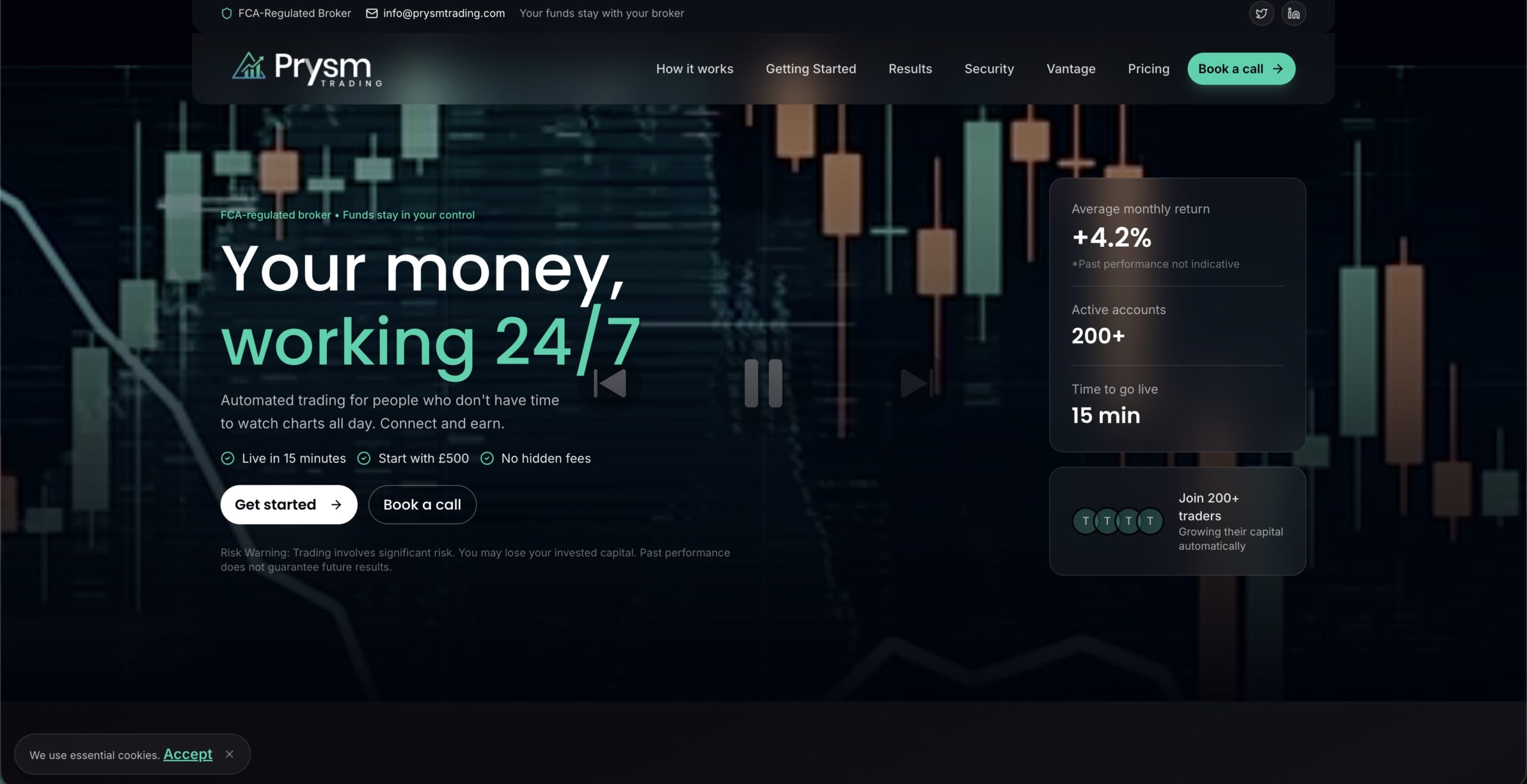

Prysmtrading presents itself as a modern automated trading solution tied to FCA-regulated brokers, promising “hands-free income” and simplified market access. But beneath the polished language and compliance claims lies a serious regulatory contradiction and documented warning flags that demand scrutiny, not trust.

This is not about speculation. It is about verified regulatory alerts and structural inconsistencies that consistently appear in high-risk investment schemes.

Regulatory Reality Check: FCA Warning Overrides Marketing

The most important fact comes from the UK financial regulator itself.

The Financial Conduct Authority has issued a warning stating that Prysm Trading is not authorised and may be providing financial services illegally in the UK. (FCA)

That single point changes everything.

If a firm claims FCA connection but is simultaneously flagged as unauthorised, one of two things is true:

- The firm is misrepresenting its regulatory status

- The structure is being used in a way that avoids direct regulation

Either way, investor protection mechanisms do not apply.

No ombudsman access. No compensation scheme. No guaranteed recourse.

The Core Contradiction: “We Don’t Hold Funds” Isn’t Protection

Prysmtrading’s model relies on a familiar argument:

- “We don’t custody your money”

- “Funds stay with regulated brokers”

- “We only provide software or signals”

On paper, this sounds safer.

In practice, it often creates a responsibility gap:

- The broker holds funds, but strategy access is controlled by a third party

- Users follow automated execution they don’t fully understand

- Accountability becomes fragmented across entities

This structure is frequently used in copy-trading ecosystems where users believe they are protected because funds sit with a regulated broker—while the actual risk control layer is unregulated.

The key question is not where funds sit. It is:

Who controls the trading decisions that generate profit or loss?

Profit Claims vs Market Reality

Prysmtrading references “average monthly returns” and “consistent performance.”

Any system that implies stability in returns inside leveraged markets must be treated as mathematically suspicious unless independently audited across long time horizons.

Here’s the uncomfortable reality:

- Markets are non-linear

- Strategy performance degrades over time

- Volatility regimes shift unpredictably

- No algorithm maintains stable monthly returns indefinitely

When platforms present smooth performance curves, the typical possibilities are:

- Short performance window selection

- Survivorship bias in reporting

- Simulated or backtested results presented as live outcomes

None of these are inherently illegal—but they are misleading when used as marketing anchors.

Withdrawal and Control Risk: The Real Stress Test

Even when platforms advertise “full withdrawal control,” the real test is behavior under stress conditions:

- Large withdrawal requests

- Profitable accounts

- High-volatility periods

This is where issues typically appear in similar systems:

- Delayed processing under “verification” claims

- Temporary account restrictions during profit withdrawal attempts

- Dependency on third-party broker support queues

- Conflicting responsibility between platform and broker

A key pattern in comparable schemes is simple:

Deposits are frictionless. Exits are not.

That asymmetry is what defines risk.

Regulatory Structure Weakness: The Hidden Gap

Even when a partner broker is regulated, the overlay platform may not be.

This creates a layered structure:

- Regulated broker handles execution

- Unregulated platform controls strategy access

- User assumes combined protection that does not legally exist

This is not theoretical. It is a known structural weakness in copy-trading ecosystems that regulators repeatedly warn about.

In essence, regulation protects execution—not necessarily the strategy layer sitting on top.

Marketing Language Red Flags

Certain phrases consistently appear in high-risk automated trading systems:

- “Set and forget income”

- “Institutional-grade returns for retail users”

- “No experience required”

- “AI-driven consistent profits”

Each of these is designed to reduce cognitive resistance.

The psychological objective is not education—it is conversion.

The critical issue is not whether automation exists. It is whether automation is being used to oversimplify risk into a passive experience.

Behavioral Pattern Comparison (Why This Looks Familiar)

When you compare Prysmtrading-style models with known scam patterns, several overlaps appear:

- Heavy reliance on “connected to regulated broker” narratives

- Emphasis on automation removing user responsibility

- Performance framing based on selective historical results

- Complex structure that diffuses accountability

- Regulatory warning or absence of clear authorization

Academic and enforcement analysis of similar systems consistently highlights that fragmented accountability is a major vulnerability exploited in online trading fraud ecosystems. (arXiv)

The structure itself is the risk amplifier.

Investor Protection Reality: What Actually Matters

Forget marketing claims. Real protection comes down to four verifiable elements:

- Direct regulation of the entity controlling trading logic

- Transparent audit history of live performance

- Clear withdrawal autonomy without platform dependency

- Single accountable legal jurisdiction

If any of these are missing or split across multiple entities, your protection becomes theoretical.

Stress Test Questions You Should Be Asking

Before engaging with any system like Prysmtrading, force clarity on:

- Who is legally responsible for losses caused by strategy execution?

- Can I independently verify live performance history over years, not months?

- What happens if the strategy provider disappears but the broker remains?

- Is there a regulator supervising the strategy layer or only the broker?

- Can withdrawals be processed without approval from the platform layer?

If answers are vague or split between entities, risk is structurally embedded.

Final Assessment: Why This Structure Is High-Risk

Prysmtrading is not evaluated as a traditional broker. It is a layered automated trading system built on:

- External broker dependency

- Unclear regulatory perimeter for the strategy provider

- Performance-based marketing claims

- High reliance on trust in automation

The core issue is not whether trading automation works. It is whether accountability exists when it fails.

When regulation covers only part of the system, users are exposed to gaps that cannot be resolved after funds are deployed.

Stay-Away Conclusion

Prysmtrading operates in a structurally fragile zone: part regulated ecosystem, part unregulated automation layer. That combination is exactly where investor misunderstandings become financial losses.

The FCA warning alone removes any ambiguity about safety in the UK context. Beyond that, the structural design introduces accountability gaps that cannot be fixed by performance claims or broker partnerships.

The rational position is simple:

If responsibility is fragmented, protection is weakened. If regulation is partial, risk is full. Avoid exposure where oversight does not cover the actual decision-making system controlling your funds.